Teasing out the Fed’s Big Plan for our Future

We live in a time of intense scrutiny and declining trust in public institutions around the world. At the Fed, we are committed to working hard to build and sustain the public’s trust. The Fed has special responsibilities in this regard. Our monetary policy independence allows us to serve the public without regard to short-term political considerations, which, as history has shown, is critical for sound monetary policymaking. But that precious grant of independence brings with it a special obligation to be open and transparent, welcoming scrutiny by the public and their elected representatives in Congress. Only in this way can the Fed maintain its legitimacy in our democratic system.

—Jerome Powell, The Federal Reserve

In his recent speech, Fed Chair Jerome Powell says the Fed, out of an interest in openness, is planning to hold town-hall meetings around the country this year in order to review where it should go with policy in the future.

Today I will explore some important features of normalization and then turn to what comes after.

This article will focus on the “what comes after†in order to explore what hints Powell gives of changes in how the Fed and the nation’s monetary system will operate. These changes might not necessarily be big, given that the Fed has moved at glacial speed in the past:

The review may or may not produce major changes…. The process is more likely to produce evolution rather than revolution…. We seek no changes in law and we are not considering fundamental changes in the structure of the Fed, or in the 2 percent inflation objective.

Powell says the Fed needs to change because the Great Recession permanently changed the world to such a degree that a new norm is one thing that is certain in his view:

In some ways, we are returning to the pre-crisis normal. In other ways, things will be different. The world has moved on in the last decade, and attempting to re-create the past would be neither practical nor wise.

While he started out by saying the changes in the Fed might not be large, it sound as though he is thinking they probably will be:

While there is a high bar for adopting fundamental change, it simply seems like good institutional practice to engage broadly with the public as part of a comprehensive approach to enhanced transparency and accountability.

“Fundamental change” is big change. It’s change at the foundational level in how the Fed operates. Whether the changes that develop through these town-hall meetings wind up being large or small, Powell claims more transparency is in order as these changes are explored.

The cynic in me is inclined to believe Powell is already planning major changes and that the town-hall meetings are intended to get the public to buy in to those changes. In the very least, it appears Powell is anticipating the possibility of changes that will require “openness and transparency” if they are going to be publicly accepted.

While I dislike the Fed as much as the next guy, I’m going to resist in this article assuming the Fed means the worst or has some veiled agenda. I want to see where Powell’s words naturally lead and avoid an easy mistake people make of reading their own biases into the words they are responding (bias confirmation). So, with my cynical disclaimer aside …

One of the things I find interesting in Powell’s speech is the insight it provides as to why the Fed has long preferred maintaining inflation at 2% when inflation (as I’ll get to) is inherently a banker’s worst enemy. Here Powell gives a big clue:

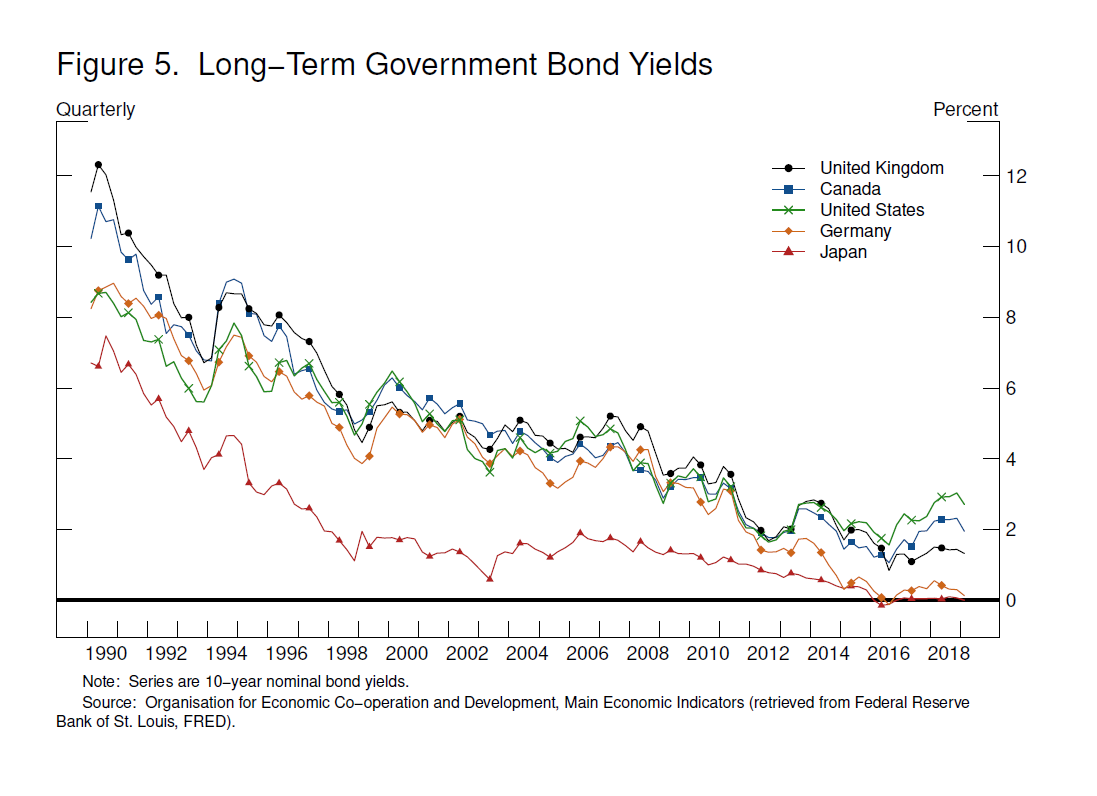

Because interest rates around the world have steadily declined for several decades, rates in normal times now tend to be much closer to zero than in the past (figure 5).8 Thus, when a recession comes, the Fed is likely to have less capacity to cut interest rates to stimulate the economy than in the past…. Persistently weak inflation could lead inflation expectations to drift downward, which would imply still lower interest rates, leaving even less room for central banks to cut interest rates to support the economy during a downturn.

Banks are OK with some inflation so long as it remains highly predictable. All interest on debt has to calculate in the cost of annual inflation in order to make real money. So, a target inflation rate of 2% pushes all interest everywhere automatically up 2% above what the buyers of debt want as profit for their risk. No one makes money off that 2% because it represents a loss of real value in money. That’s where a managed target of 2% is preferable to banks who can trust the Fed will hold there, enabling them to figure out what total interest they need to charge to cover their other costs and leave a real profit over time.

What I’ve wondered, though, is why the Fed wants any inflation at all. Why not just target a predictable 0%. Powell says the reason is to build a buffer into interest all across the credit spectrum so the Fed has some built-in room to lower interest rates. Maintaining inflation at 2% usually assures interest rates will stay well above that level, giving the Fed some room to maneuver without causing real rates to go negative.

Just over 10 years ago, the Federal Open Market Committee (FOMC, or the Committee) lowered the federal funds rate close to zero, which we refer to as the effective lower bound, or ELB. Unable to lower rates further, the Committee turned to two novel tools to promote the recovery. The first was forward guidance, which is communication about the future path of interest rates. The second was large-scale purchases of longer-term securities.

Given the desire to maintain a 2% inflation buffer and the fact that we are already so close to the lower bound, Powell states,

It is therefore very important for central banks to find more effective ways to battle the low-inflation syndrome that seems to accompany proximity to the ELB.

Powell uses that argument to start building a case for allowing inflation to run hot, which inclines me to think that one of the fundamental changes the Fed needs to get the public to accept is the possibility of higher inflation for longer:

In the late 1990s, motivated by the Japanese experience with deflation and sluggish economic performance, economists began developing the argument that a central bank might substantially reduce the economic costs of ELB spells by adopting a makeup strategy.9

A “make-up strategy†says that, if inflation has run below expectations (as was the case throughout the Fed’s Great Recovery), then it would be reasonable for Fed to allow inflation to run above expectations during the post-recovery period to “make up” the difference. That would take public buy-in because those of us who are old enough to have lived through the late Nixon and Carter years, remember how much we got pinched by high inflation.

Powell could be trying to build an argument for more QE to come because the recovery is clearly weaker than they thought it would be, and he clearly wants to back away from tightening. QE, after all, is what they tried to use to generate inflation during the Great Recovery. Their QE only inflated assets because that is where all the money went, so this raises a question of whether Powell is preparing the public for a different form of QE that will put money more directly into the general economy, such as “helicopter money.” Is he talking about town-hall meetings as a way of seeing if the public can be prepared in such a way as to not feel alarmed if inflation runs high because they will know in advance it is all part of the plan. (That way the Fed won’t become distrusted as having lost control and will be able to maintain its “independence” when inflation goes up, which was the context for his statements.)

Powell may be wanting to build a case with the public for running hot, or it could be just to build the case for permanently maintaining the higher balance sheet that has resulted from the QE the Fed has already run. Maybe he just realizes that they can never lower their balance sheet, and he wants to build a case that this does not mean the Fed has failed because it turns out not to be able to do what it has always said it would do at this juncture in the “recovery” process.

Simply maintaining its present large balance sheet would not be a large change at all from the new normal. It is the new normal, but it would be an extended change from the old normal, and Powell may be hoping to avoid criticism that says, “The Fed failed because it cannot normalize without crashing its own recovery†(which, you may note, is exactly the criticism I have been leveling at the Fed)

Perhaps that kind of criticism is getting to the Fed at a level where it feels it risks losing the public trust, which is essential to maintaining the bankers independence from too much government interference with their own self-government. I don’t think it is too much of a leap to my own bias to say that Powell’s words in context seem most likely to be leading to either the need to talk the public into accepting higher inflation as a new temporary norm so that everyone doesn’t accuse the Fed of losing control of money supply when it lets inflation run hot … or, in the very least, to accepting permanent maintenance of a large balance sheet as a new norm so that people don’t see their inability to ever reduce it as a sign that their recovery is as dependent on that continued massive liquidity as ever.

(Knowing their recovery was dependent on continued expansion of that liquidity is why I said last year the stock market would crash as soon as their balance sheet reduction got up to full velocity.)

The Fed would not need to make this shift if its Great Recovery had actually worked. In full recovery, the patient doesn’t need continued life support. What the Fed’s shift to a new norm (and to get the public to buy in to that as an actual “norm”) really proves is my longtime tenet that the Fed chose a recovery path where diminishing returns will forever require the Fed (just like Japan) to do more and more QE. Their idea that you can build enduring wealth by piling up debt was never sustainable.

As I wrote in the beginning years of all of this, you cannot solve the debt problem that blew up in 2008 by creating more debt. All you can do by that path is kick the can further down the road. However, kicking the can again once you get that far down the road will require an even greater pile of debt … and so it goes until the weight of it all finally overwhelms you.

What Powell clearly indicates a need to convince society that inflation needs to run hotter than 2%, and the public will be told this is temporary — just a makeup strategy that will end after we’ve run hot for as long as we ran cool to achieve an average of 2% over time. Given that the Fed couldn’t run hot when it tried with the old QE, one has to think that either means much higher QE or a different kind of QE is necessary to keep the economy from shrinking into recession.

Powell is certainly not unaware of the inversion of the yield curve last month or of the fact that all previous inversions in the past half a century have immediately preceded a recession — a recession each time that the Fed, itself, has now acknowledged has been caused by the Fed tightening until we get to a recession.

So, here were are where the Fed instantly stopped raising interest rates and now apparently wants to build a case for keeping its balance sheet high indefinitely, and is also building a case for running hot with inflation. They may be concerned that just stopping their balance-sheet reduction could lead to inflation (always the big fear of a high balance sheet / high money supply) as the money that went to stocks and bonds slowly seeps into the general economy. That would explain why they are tapering their curtailment of balance-sheet reduction over a period of months, rather than just stopping it cold. In which case, Powell needs to build the case for higher inflation targets as being the new plan, rather than the failure of the former plan before he can end quantitative tightening (QT).

In the event of a recession anytime soon, Powell has reason to fear he will need to re-expand the balance sheet to get us back out of a recession because he knows (as he just averred) that he has very little room to lower interest rates as a means of getting us out of a recession.

Bear in mind the lag time between Fed action and actual response in the overall economy (as opposed to response in stock and bond markets) is about half a year. So, if the Fed kept raising interest for too long, recession from overtightening won’t hit until summer, given that their last raise (the one everyone thought was too much) was in December. Without much room for the interest-rate-reduction “tool†Powell mentioned, he will need to go back to the quantitative-easing “tool.†So, he has a lot of case building to do if he is going to return to QE without killing public trust in the Fed should it drive inflation above the Fed’s long-stated target.

This is EXACTLY the situation I said the Fed would be in as soon as it tried to normalize policy — that it will have to return to QE but will not be able to without breaking public trust in the Fed, without which trust, the Fed’s money becomes worthless.

So, here we are. Powell acknowledges the Fed’s independence (which really means the big bankers’ free rein over the monetary system) is at risk. He acknowledges that the Fed will have to engage in a lot of public discussion in order to maintain the trust that is necessary for the government to continue to give bankers total control over the money supply and over what actually is money.

The need to maintain a high balance sheet by itself indicates the Fed never could play out its promised end game, so a need to actually raise the balance sheet after having just tried unsuccessfully to reduce it will certainly cause people to doubt the Fed knows what it is doing. (It proves, as I’ve claimed all along, the Fed never had an end game that worked.)

The the Fed has to start changing public opinion now to accepting all of that — higher inflation because of a re-expanding balance sheet at a time when it cannot lower interest much without going negative — as the new norm. That interpretation fits perfectly with what he goes on to say:

If a spell with interest rates near the ELB leads to a persistent shortfall of inflation relative to the central bank’s goal, once the ELB spell ends, the central bank would deliberately make up for the lost inflation by stimulating the economy and temporarily pushing inflation modestly above the target.

In other words, “Prepare for more QE as the new norm.â€

If households and businesses are confident that this future inflationary stimulus will be coming, that prospect will promote anticipatory consumption and investment.

And there it is. Instead of just forward guidance to investors in stocks and bonds, as the Fed has been doing, part of the plan now is forward guidance to households in order to turn the threat of inflation from more money printing and low interest at the ELB into pressure to consume now because inflation means you’ll get less in the future. That, in itself, will both stimulate the economy and cause inflation. (That is probably another reason the Fed likes to maintain 2% inflation — to drive people to consume, rather than save for the future because whatever you want only gets more expensive if you wait. So, it pressurizes the economy.)

In other words, “So long as we can convince you that inflation above our long-stated target is temporarily justifiable on the basis that it has long remained below our target, we can really ramp up the QE, and that will drive stocks up once again, and people will buy now (knowing it will cost them more to wait and buy later) on the basis that their money is going to be worth less later on.â€

And THAT is how you push people to go even beyond their current high debt. Make it more expensive to wait and buy later by suppressing interest and inflating prices. Think about what a desperate game that is for maintaining the illusion that the Fed knows what it is doing and that its plans are still working. It’s even more desperate when you consider that bankers are supposed to hate high inflation because it erodes their profits on all that credit they’ve already issued. (Of course, we’ve now learned that banks don’t have to worry much about making profit off the credit they’ve issued now that they can make profits by getting vaults full of quantitatively easy money to invest in stocks and bonds! That is where the end of Glass-Steagall got us. Banks can make even more money investing than loaning. That, too, has become the new norm. So, banks will tolerate a little higher inflation (devaluation of their proprietary product — money) if it allows them to return to the QE investment game — the prospect that “will promote … investment.â€

The make-up strategy, if the public can be consoled into accepting it as the new norm, will work like this:

The central bank could target average inflation over time, implying that misses on either side of the target would be offset…. Some kind of makeup policy could be beneficial.

So, there you go: the case is clearly being built for higher inflation targets that will be necessary if the Fed is going to launch into more QE because, as I’ve warned for years, the next round of QE after the Fed attempts normalization and fails will have to be larger than anything we’ve seen before due to the law of diminishing returns that we’ve already seen at play in previous rounds.

We have to push forward an even greater pile of debt — keep plowing the snow straight ahead into a bigger and bigger mountain, instead of off to side until we can no longer push it forward.

One might ask why the Fed and other major central banks chose not to pursue such a policy.13 The answer lies in the uncertain distance between models and reality. For makeup strategies to achieve their stabilizing benefits, households and businesses must be quite confident that the “makeup stimulus” is really coming.

No, I think what Powell really means is that households must be made confident they they will work after it became obvious that the Fed’s last recovery plan failed when it started to die as soon as the Fed removed life support. Households, in fact, must be readied for the coming of inflation (for which “makeup strategy” is a euphemism) so they don’t move to distrusting the Fed’s competence by realizing the Fed has been inept all along.

Powell stated off by acknowledging his fear that the Fed now seriously risks losing confidence and that it does, as a result, also seriously risk having its long-standing independence stripped away from it by a government that will have to rise to public outcry if the outcry grows strong enough; or the pitchforks and torches will be coming out, and politicians will be hung on the gallows of the election booth (or something worse if that doesn’t work).

By teasing out the what Powell is saying based on the context in which he couched all of it, we can now understand why the Fed didn’t just slam the brakes on its balance-sheet reduction and go right back to expanding the balance sheet with more QE.

Powell’s words sound cautions, maybe even a touch afraid that the public may have a deep memory instilled in those of us who are old enough to remember the pain that even a little runaway inflation (just double-digit inflation in the teens) causes. We experienced that in the Nixon era, and it was not pleasant. The Fed has to convince people that it can control inflation from running away before it implements these amped-up inflationary moves that will be necessary to push us out of the next recession. They have to be assured this is just a temporary adjustment.

(Of course, it will require new rounds of even higher adjustments later, but the Fed probably continues to believe one more round of its QE policy will finally work, just as Japan does. But it doesn’t work. It’s not sustainable. It always has to ramp up, like any Ponzie scheme, to a higher tier.)

Without the town meetings to prepare the public, fear of inflation could cause people (horror of horrors) to flee the Fed’s fiat money and run to gold and other precious metals — the Fed’s only serious competitor — or to the Fed’s newest competitor — digital money that is not owned and controlled by the banks! Yikes!

So, here we have it:

In [make-up strategy] models, confidence in the policy is merely an assumption. In practice, when policymakers considered these policies in the wake of the crisis, they had major questions about whether a central bank’s promise of good times to come would have moved the hearts, minds, and pocketbooks of the public. Part of the problem is that when the time comes to deliver the inflationary stimulus, that policy is likely to be unpopular.

Indeed! This is a big moment in which the Fed now, in the very least, sees and fears a crisis could build. I don’t know if I can go so far as to say it believes one will build; but Powell is clearly concerned that the Fed must be proactive in steering away from it:

My FOMC colleagues and I believe that we have a responsibility to the American people to consider policies that might promote significantly better economic outcomes.

Better than what? Better than what might happen if a “make-up strategy” is employed and the public panics by hoarding gold or by running to digital currencies the Fed doesn’t control? Or better than what the Fed’s Great Recovery program delivered where the wealth was disproportionately distributed almost entirely to those who were already wealthy? (To avoid that, they have to make sure the money gets into the hands of households, which is where it is certain to become inflationary — otherwise known as “helicopter money” because new money is fed into the economy in a way that is more like just dropping buckets of cash into the streets from a helicopter. Or just better than can be had by trying again to lower interest rates in an environment where the Fed no longer has much room to lower them back down (because it never gained the headroom it wanted to before it had to stop) without going negative and where diminishing returns are making interest reductions less effective?

Let’s be clear that inflationary strategies really are the main plan the Fed has in mind:

Makeup strategies are probably the most prominent idea and deserve serious attention. They are largely untried, however, and we have reason to question how they would perform in practice.

Oh, good. The last recovery made up of the biggest untried monetary experiences in US history was not effective, so now we have to experiment with more desperate untried policies. God forbid we actually make the kind of huge economic changes in the foundation of our economy that we really need in order to get out of this delirium. (See my “Ideas for Change” section.)

Before they could be successfully implemented, there would have to be widespread societal understanding and acceptance–as I suggested, a high bar for any fundamental change. In this review, we seek to start a discussion about makeup strategies and other policies that might broadly benefit the American people.

Trickle-down economics compounded

Yes, we just convince the American people that a little higher inflation is good for people who’s wages never rise. It is not enough that you’re income remained flat for decades, we must now make sure prices rise faster, too. Never mind that the little guys knows this means our retirement investments, which were damaged in the last two crises and which lost the opportunity for safe yields during the Fed’s Great Recovery also now get inflated away in value.

If I am generous, I am inclined to think the Fed rationalized their last policy under belief that creating money in the hands of the rich actually would benefit all of society. It’s not hard to see how they could believe that. After all, don’t the many conservatives who have adopted trickle-down economics as somehow being a conservative position (don’t ask me why it would be) readily believe that giving money to the rich first and letting it trickle down to the rest is the best way to create wealth? We have half a nation full of people who seem believe that as an article of faith in spite of 35 years that prove it doesn’t.

Of course, it is highly likely the Fed will be wrong in what it believes because 1) they are dumb like that; 2) they are rangebound in their thinking to believe all solutions must serve bankers first just like Republicans are rangebound to thinking all financial solutions must serve the rich first and then trickle down to the lower 99%.

(Don’t worry, I plan to give Democrats just as much criticism as I continue my discussion about Socialism and Modern Monetary Theory (MMT). So, if you’re a Republican don’t run, because both parties deserve criticism for the mess that has evolved under their watch.)

It is certainly fair to conclude the Fed now thinks we need a bigger solution than what has been tried and that it is something so big that it will take broad societal discussion to pave the way for it. While Powell says he is concerned about Fed independence, he is also acknowledging that its independence will only be tolerated if the public is allowed to “scrutinize” the Fed’s plans and to participate in the conversation about where society goes from here. I don’t think the Fed has ever felt the need to make a change so big or so naturally opposed by the public that it advocated broad public discussion as essential before proceeding.

In the very least, these town-hall meeting will help the Fed craft its language and its approach to what the public will accept via smaller focus groups.

At the end of his speech, Powell drops back to reassuring everyone that the economy is beautifully healthy right now. He has to do that, regardless of the truth, because a talk like this about large future changes risks causing an immediate panic now:

With nothing in the outlook demanding an immediate policy response and particularly given muted inflation pressures, the Committee has adopted a patient, wait-and-see approach to considering any alteration in the stance of policy.

Well, that and adopting numerous town-hall meetings to consider “fundamental†policy changes so great the Fed must get these ideas accepted before it implements them.

Considering monetary policy more broadly, we are inviting thorough public scrutiny and are hoping to foster conversation regarding how the Fed can best exercise the precious monetary policy independence we have been granted. Our goal is to enhance the public’s trust in the Federal Reserve–our most valuable asset.

Their “most valuable asset” being trust in their money.

Banks hate it when debt gets inflated away. Rapid inflation (the kind that inflates away debts) is a banker’s worst fear at night. It is this innate fear of runaway inflation that causes the Fed every time to err’ on the side of tightening right into recession. While it wants to create as much money as it can because all new money is issued through bank loans, creating too much leads to runaway inflation, which makes that money worth less. Then people don’t trust it, so it becomes worth less still until it is just worthless.

The Federal Reserve is nothing but a consortium of private bankers mixed with a few mostly cherry-picked government appointees in order to assuage the government’s concerns about giving bankers total control of the national currency. Bankers are creditors, and bankers never do anything at their expense! So, they would not be talking about the need to run inflation a little hot if they didn’t have to.

The Fed also has no desire to inflate away government debt. Bankers are only the government’s friend in the same way that a mosquito is your arm’s best friend. Through government debt, bankers OWN the government. However, they do have to make sure the government’s debt remains manageable because the government can easily strip their ownership of the monetary system away since the government created that chartered ownership in the first place. That is what the Fed is talking about when Powell repeatedly brings up the Fed’s cherished “independence.”

That means, the Fed cannot raise interest higher, or they’ll cause problems for the government. The Fed must work with the government enough to accomplish the government’s objectives (serve the government obsequiously) if it is going to retain ownership of the world’s primary currency because it is not just public trust that is their highest asset but political trust.

So, the Fed has tightrope to walk all the time. No bankers seek to make their own assets worthless just to placate the government; but the government has piled up so much debt and is now piling it up so much faster that higher interest is impossible, and stopping at the current level as the Fed just did and running down the balance sheet, which largely holds government debt, creates a high risk of higher inflation. So the rope is getting thinner.

What are the “other policies” of which Powell hints?

I’m going to speculate now on what those vague other policies Powell mentioned might be since he gave no clue.

One of the things pressing the Fed hard from behind is MMT. Modern Monetary Theory, which I’ll go into in a future article, in essence says the Fed can create as much money (digital or non-digital) as the government needs in order to finance everything the government would love to do so long as it stays within inflation boundaries. Powell has spoken openly against MMT as a bad idea, and the Fed has always been hyper concerned about maintaining inflation but moderating it.

MMT is the one theory most likely to create hyper-inflation. While the Fed may want some inflation, it fears hyper-inflation because it makes it impossible for banks to feel secure in making loans to anyone, as they will likely be repaid in money is worthless. It destroyed the Fed’s proprietary product — the US dollar.

The Fed’s Great Recovery program, however, has created an environment where a backlash is developing in society on a broad level because of the chasm it created between the haves and have-nots. One answer Democrats are starting to turn to is MMT as well as Socialism. Banksters only like to socialize their losses. Beyond that, they want full Capitalist control.

MMT is the funding mechanism for Alexandria Ocasio-Cortez’s grand ambitions of the Green New Deal and for Bernie Sanders Socialist solutions, such as universal health care. It is a must for funding those adventures. So, whether MMT is inherently Socialist or not, it is closely tied to Socialist thought in America, and is probably for that reason perceived as a big threat by big Capitalist banksters.

The Fed may be in a hazy way realizing that it has created this backlash, given that Yellen spoke out about her concern over disproportionate distribution of wealth that was developing under the Fed’s Great Recovery program. It is unclear whether Yellen was genuinely concerned and just too range-bound in her thinking to realize the Fed was the cause of this disproportionality or whether she knew the Fed was the cause but was clueless as to how to avoid it because she is rangebound to thinking that all solutions must trickle down through banks or if she was just pretending to be concerned because she had to maintain the illusion that the Fed cares about the general public in order to maintain that trust that that is essential Fed independence.

I can be generous to think she is actually the caring grandma she appears to be and is just blinded by her years inside the banking system’s entrenched school of thought that only sees financial answers as having to come from banks and as having to be good to banks in order to be good to the people because people need banks.

I have always said here that the Fed may just be oblivious due to its own group think. MMT probably does have the Fed on a run to find a better solution before that one is imposed by the new democrats (which will soon become the New Democrats — a party name — if the traditional Democrats don’t start embracing these Socialist ideals, whether the old realize that or not).

For those who lean more conspiratorial, here is another contender for those “other policies” the Fed will be considering:

MMT is not the Fed’s only threat. Loss of its greatest asset — public trust — will ultimately cause the public to move to exchange mechanisms the Fed has no control over, such as gold or digital currency. Gold (and all other precious metals), the Fed manages to control by owning enough of it that they (and their central-bankster pals) can throw a bunch off as ballast in order to crash gold prices if gold starts getting too competitive.

So far, however, the Fed has NO control over digital currencies. That’s a real threat. Digital currencies are pressing the Fed from behind even more intensely than MMT is, which is why I think I need to bring them up here.

One solution — since the Fed has no power to stop the public interest in digital currencies — is for the Fed is to go with the flow but gain control over that argument by gaining full control over digital currency. That would require a huge number of “town-hall meetings†to convince the public that it is in the “best security interest of the American people†to let the Fed issue the ONLY legal digital currency in order to avoid some of the scandals we’ve already seen (more of which are certain) There are bound to be some digital currencies that aren’t anything other than a digital Ponzi scheme.

The Fed would have to acquire that power from the government, and that means it must first win the public argument because right now the public is dead-set against the Fed seizing control over digital currencies. It will also have to convince the government that Fed control is a security need for the government.

That means a switch to digital currency certainly would require broad discussion and much preparatory groundwork, but it would also give the Fed more independence, which is another reason I bring it up here, given that Powell brackets his entire speech by focusing on the primary importance of Fed independence.

Digital currency would actually give the Fed much more control than it has over cash that floats to unknown whereabouts or that could have simply been destroyed in the explosion of a getaway car or a downed plane without the Fed even knowing anything happened to it.

While there is nothing in Powell’s words about digital currency, he clearly is anticipating a big untried solution that will need society’s buy-in. Existing grassroots digital currencies are a far bigger threat than MMT because MMT still includes the Fed in creating all the money; it just gives the government more control over the size of money supply.

Loss of trust in the Fed would move the already digitally oriented masses toward digital currencies, so it’s not hard to see how that would be the Fed’s biggest concern should it lose its “most important asset.” Still, the switch to digital currency controlled by the Fed would require huge public persuasion because a lot of older people fear it.

A strategy for convincing the government is to emphasize how digital currency will make tax evasion harder. (They’ll say “impossible.”) They will petition the government to allow only one digital currency under Fed rule to avoid counterfeiting, which devalues their physical currency, and to establish total control over money supply for reasons of helping the government manage the economy more directly and to avoid tax evasion and to curtail crime. After all, unregulated digital currencies have been accused of working very nicely for laundering illegally made money.

Of course, anything man can make, man can break; so their new system will always be vulnerable to counterfeiting by hacking and to theft by hacking and to the bank’s own abuse of power and to all kinds of problems we haven’t even though of yet; but that is material for other conversations down the road.

Occam’s alternative to all the above

The Fed fears digital systems only to the extent they don’t own, control or benefit from them directly and fears MMT becoming a government dream as a way of financing endless government projects because that is the path to hyperinflation.

An alternative to the idea that the Fed is looking to manage those concerns is as simple as the possibility that the Fed doesn’t have a solution for the corner it has painted itself into, so it wants to foster broad public discussion in order to try to distill one. It may have ideas that it wants to run up the flagpole to see if one flies, which means it has to have some “other policies†to bring up if the higher inflation falls like a ton of bricks, or it may be looking for other policies to be suggested by the public.

That possibility covers the same contextual concerns Powell repeatedly expresses about need for public discussion and the risk of losing public trust and losing Fed independence because the realization that the Fed simply doesn’t have a clue about what went wrong or where to go from here ought to be as disconcerting as any of the above.

{kind=link}

Leave a Reply